Balance Transfer Cards for Debt Consolidation: A Guide to 0% APR Strategies

Credit card debt has a way of growing quietly. A balance that started as a manageable expense can become a financial burden after months of high interest charges. Many cardholders focus on making minimum payments without realizing how much of each payment goes toward interest rather than principal.

One of the most effective tools for reducing interest costs is a balance transfer credit card with a 0% introductory APR. Used correctly, it creates breathing room, accelerates debt repayment, and simplifies finances. Used incorrectly, it can lead to new debt and additional fees.

After reviewing hundreds of debt reduction strategies and credit products, one pattern appears repeatedly: people who understand the mechanics of balance transfers save significant amounts of money, while those who focus only on promotional offers often miss the real opportunity.

This guide explains how balance transfer cards work, how they compare with other forms of debt consolidation, and how to determine whether this approach fits a particular financial situation.

What Is Credit Card Debt Consolidation?

Credit card debt consolidation combines multiple credit card balances into one account or one payment structure. The goal is simple: reduce interest expenses, simplify repayment, and create a clearer path toward becoming debt-free.

Several methods exist for credit card debt consolidation.

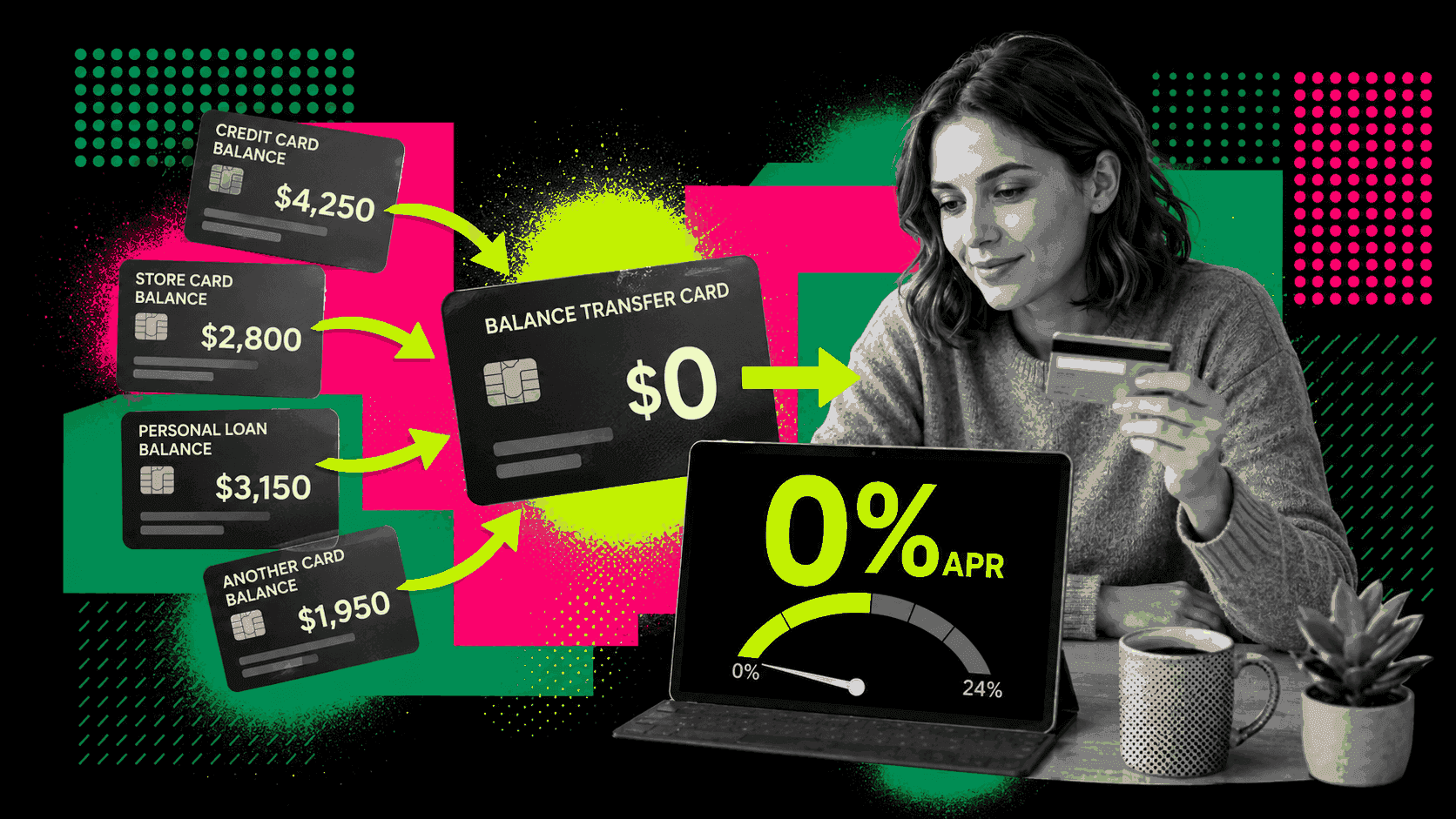

A borrower may transfer balances from several cards to a new balance transfer card offering a promotional 0% APR period.

Another option involves a personal loan. Some consumers search for a credit card consolidation loan when they want fixed monthly payments and a predictable payoff schedule.

Homeowners sometimes use home equity products, although this approach introduces additional risks because unsecured debt becomes secured by property. Among these options, balance transfer cards remain one of the lowest-cost solutions for qualified borrowers because they eliminate interest charges for a limited period.

How Balance Transfer Cards Work

A balance transfer card allows existing debt to move from one credit card issuer to another. The new card typically offers a promotional interest rate of 0% for a defined period, often between 12 and 21 months.

Instead of paying interest at 20%, 25%, or even higher rates, every dollar paid during the promotional period reduces the principal balance.

Consider a consumer carrying $10,000 in credit card debt at a 24% APR. Interest charges alone can consume hundreds of dollars every month. Moving that balance to a 0% APR card redirects those funds toward reducing debt rather than servicing interest.

Most issuers charge a balance transfer fee ranging from 3% to 5% of the transferred amount. Even after accounting for that fee, the savings frequently exceed the cost when compared with paying high interest for another year or more.

The key is treating the promotional period as a deadline rather than a temporary discount.

Credit Card Consolidation vs. Personal Loan Consolidation

Consumers researching debt solutions often compare balance transfer cards with personal loans. The choice depends on several factors, including credit score, debt amount, repayment timeline, and financial discipline.

A balance transfer card works best when debt can be repaid before the promotional period ends. The primary benefit is the possibility of paying no interest during that period.

A credit card consolidation loan offers a different advantage. The borrower receives a fixed repayment schedule, a fixed interest rate, and a clear payoff date. Monthly payments remain predictable throughout the life of the loan.

For individuals carrying moderate balances and strong credit profiles, a balance transfer often produces lower total borrowing costs. For those carrying larger balances that require several years to repay, a personal loan may provide more structure and stability.

What Is Credit Card Refinancing?

Many consumers encounter terms such as credit card refinancing and wonder whether they differ from debt consolidation. The concepts overlap significantly.

What is credit card refinancing? In simple terms, it involves replacing existing credit card debt with a new financing arrangement that offers better terms.

Those better terms usually include:

- Lower interest rates

- Lower monthly payments

- Simplified repayment

- Faster debt elimination

What does credit card refinancing mean in practical terms? It means reducing the cost of carrying debt. What does credit card refinancing mean for a borrower struggling with high-interest balances? It means finding a more affordable path to repayment.

Balance transfers represent one form of credit card refinancing. Personal loans also fall into the broader category of refinancing credit card debt.

How to Refinance Credit Card Debt Using a Balance Transfer

People frequently ask how to refinance credit card debt without taking out a loan. A balance transfer provides a straightforward answer.

The process starts with evaluating current balances, interest rates, and credit scores. The next step involves comparing available balance transfer offers. Once approved, the borrower transfers eligible balances to the new card. The old accounts remain open unless there is a strategic reason to close them. After the transfer is complete, the focus shifts entirely to repayment.

The best way to refinance credit card debt through a balance transfer is to divide the total balance by the number of promotional months available. If the transfer fee is added to the balance, the repayment plan should include that fee. For example, transferring $12,000 with a 3% balance transfer fee creates a total balance of $12,360. To repay it over 18 months, the borrower would need to pay about $687 per month. Following that schedule eliminates the debt before interest charges begin.

Failure to create a payoff plan remains the most common reason balance transfer strategies fail.

Advantages of Balance Transfer Cards

The strongest benefit is obvious: temporary elimination of interest charges. That benefit creates several secondary advantages.

First, debt repayment accelerates because every payment reduces principal.

Second, financial management becomes simpler. Multiple balances become a single account.

Third, reduced credit utilization may improve credit scores over time if balances decrease consistently.

Fourth, lower interest costs free cash flow for emergency savings and other financial priorities.

For consumers carrying several high-interest balances, the consolidation of credit card debt into one account often reduces stress and improves financial visibility.

Instead of tracking due dates across multiple cards, attention remains focused on a single repayment objective.

Potential Risks and Drawbacks

Balance transfers are powerful tools, but they are not risk-free.

The most significant danger appears when borrowers continue using their old credit cards after transferring balances. A person who transfers $8,000 and then accumulates another $5,000 in new debt has not solved the underlying problem. Total debt has increased rather than decreased.

Another issue involves promotional expiration dates. Once the introductory period ends, the remaining balance becomes subject to the card's standard APR. That APR may exceed 20%.

Transfer fees also deserve consideration. A 5% fee on a $10,000 transfer equals $500. The fee often remains worthwhile compared with ongoing interest costs, but it should be included in any savings calculation.

Approval requirements present another challenge. The strongest offers generally target applicants with good to excellent credit. Consumers with lower credit scores may receive shorter promotional periods or lower transfer limits.

Who Should Consider a Balance Transfer?

Balance transfer cards tend to work best under specific circumstances.

The ideal candidate carries high-interest credit card debt, maintains a solid credit profile, and possesses sufficient income to eliminate debt during the promotional period. This strategy is particularly effective when balances remain manageable relative to monthly income.

Someone carrying $5,000 to $15,000 in credit card debt often benefits substantially from a well-executed transfer strategy. The approach becomes less effective when debt levels are so high that repayment within the promotional window becomes unrealistic. In those cases, a credit card consolidation loan or another structured repayment solution may deserve consideration.

Calculating Potential Savings

A quick comparison reveals why balance transfers attract so much attention. Assume a borrower carries $15,000 at a 25% APR. At a 25% APR, a $15,000 balance generates roughly $3,750 in annual interest if the balance remains unchanged. Actual interest charges will vary because card issuers typically calculate interest using the average daily balance and because payments reduce the balance over time.

A balance transfer card charging a 3% transfer fee would cost $450 upfront. Even after paying the fee, potential savings exceed $3,000 during the first year alone. The exact numbers vary based on repayment speed and promotional terms, but the principle remains consistent. High-interest debt creates a significant drag on financial progress. Eliminating interest for a limited period changes the math dramatically.

Common Mistakes During Credit Card Debt Refinancing

Credit card debt refinancing succeeds when borrowers avoid several predictable mistakes.

The first mistake involves making only minimum payments.

The second involves missing a payment. Many issuers reserve the right to terminate promotional terms after serious payment issues.

The third involves continuing to accumulate new debt while attempting to eliminate existing balances.

The fourth involves transferring balances without calculating a realistic payoff schedule.

The fifth involves ignoring transfer fees and standard APRs when comparing offers.

Is a Balance Transfer Better Than a Debt Consolidation Loan?

There is no universal answer. A balance transfer generally wins when debt can be repaid quickly, and the borrower qualifies for a lengthy 0% APR period.

A loan consolidation credit card debt strategy involving a personal loan often works better when balances are larger, and repayment requires several years. The decision comes down to mathematics rather than preference.

Compare total interest costs, transfer fees, loan origination fees, monthly payment requirements, and repayment timelines. The option with the lower total cost and realistic repayment structure usually deserves priority.

Final Thoughts

Balance transfer cards remain one of the strongest tools available for reducing high-interest credit card debt. They combine debt consolidation and credit card refinancing into a single strategy that lowers borrowing costs and simplifies repayment. Success depends less on the promotional offer and more on the behavior that follows.

Consumers who create a repayment plan, avoid new debt, and eliminate balances before promotional rates expire often save thousands of dollars in interest. For many households, a properly structured balance transfer serves as both a financial reset and a clear path toward becoming debt-free.

Frequently Asked Questions

Does a balance transfer hurt credit scores?

A new credit application may cause a temporary decrease in score. Over time, reducing balances and lowering credit utilization often support stronger credit health.

Can credit card debt consolidation eliminate debt?

Consolidation does not erase debt. It restructures debt into a more manageable form and may reduce interest costs.

Is credit card debt refinancing the same as debt consolidation?

Not always. Credit card debt refinancing focuses on obtaining better borrowing terms. Consolidation focuses on combining multiple debts. Many balance transfer strategies accomplish both goals simultaneously.

What is the best way to refinance credit card debt?

The best approach depends on credit score, debt amount, and repayment timeline. Balance transfer cards often deliver the lowest borrowing cost for borrowers who can repay balances during the promotional 0% APR period. Personal loans frequently work better for longer repayment schedules.

Denis Goncharenko

Denis Goncharenko is a senior fintech analyst and financial writer with over 8 years of experience covering personal finance, consumer debt dynamics, and digital banking integration. Having a deep background in data-driven financial journalism, Denis specializes in translating complex federal lending laws, interest rate calculations (APR), and credit scoring mechanics into actionable, consumer-first guides. His analytical approach helps borrowers navigate subprime lending landscapes safely.

To author