The History of the 50/30/20 Rule: Where It Came From and Why It Stuck

The 50/30/20 rule has a precise origin: a 2005 book, two co-authors, and decades of bankruptcy research compressed into three numbers. Understanding where it came from helps you decide whether it belongs in your financial life – or whether you need something built differently.

This article is part of our deeper look at budgeting frameworks and how they compare. If you're already familiar with the basics and want to see how the math plays out for a real household, jump straight to the family budget calculation walkthrough.

Who Created the 50/30/20 Rule

Elizabeth Warren's Role

Elizabeth Warren: The Academic Behind the Formula

Before she became a U.S. Senator from Massachusetts (a seat she has held since January 2013, per senate.gov), Elizabeth Warren spent three decades studying why American families go broke. That research is the direct foundation of the 50/30/20 rule.

Her academic career ran through the University of Houston Law Center, the University of Texas School of Law, the University of Pennsylvania Law School, and ultimately Harvard Law School, where she held the Leo Gottlieb Professorship – one of the most prestigious endowed chairs at HLS. She currently holds emerita status there.

Warren's expertise was bankruptcy law, but her real subject was the middle class. She co-led the Consumer Bankruptcy Project, a multi-decade empirical study of thousands of personal bankruptcy filings. The data kept pointing to the same conclusion: the families filing weren't reckless spenders. They were ordinary households blindsided by job loss, divorce, or medical bills – with no financial buffer to absorb the shock.

That finding shaped everything she wrote, including the rule that now appears in every major personal finance app.

"By the end of this decade, one of every seven families with children will file for bankruptcy."

– Elizabeth Warren, Harvard Gazette, 2003

Her institutional authority extends beyond academia. Warren chaired the Congressional Oversight Panel for TARP – the $700 billion bank bailout program – and served as the special advisor who designed and launched the Consumer Financial Protection Bureau (CFPB), the federal agency created to protect Americans from predatory financial products.

When Warren wrote about household budgets, she wasn't theorizing. She had read the court filings.

Amelia Warren Tyagi: The Business Mind Behind the Method

Amelia's Specific Contribution to the Concept

Amelia Warren Tyagi is Elizabeth Warren's daughter and the co-author who translated academic bankruptcy research into a framework a working family could actually use on a Tuesday night.

Her credentials are distinct from her mother's. Tyagi holds an MBA from the Wharton School of Business and worked as a management consultant at McKinsey & Company. She later co-founded Business Talent Group (BTG), a marketplace connecting independent consultants to corporate projects, and co-founded Demos, a progressive policy think tank.

That combination – Wharton training, McKinsey rigor, and entrepreneurial experience – is what turned Warren's empirical findings into a three-bucket system with specific percentages. In a 2007 BusinessWeek interview, Tyagi explained that the collaboration worked precisely because it fused her business consulting lens with her mother's academic research on bankruptcy patterns.

The Publishers Weekly review from April 2005 confirmed both women as co-architects of the strategy, not just co-bylines on a cover.

Their earlier collaboration, The Two-Income Trap (2003), had already argued that two-income households were paradoxically more financially fragile because both paychecks were fully committed to fixed costs – mortgage, childcare, car payments – leaving nothing for income shocks. All Your Worth was the practical answer to that structural problem.

The Book That Launched the Rule: All Your Worth (2005)

The Economic Context That Made the Book Necessary

Warren and Tyagi published All Your Worth: The Ultimate Lifetime Money Plan (Simon & Schuster, 2005) into a specific American economic moment – and that context explains why the formula resonated so widely.

Between 2000 and 2005, U.S. household debt grew sharply, driven by low post-recession interest rates and aggressive mortgage lending. The Federal Reserve's Survey of Consumer Finances for 2001 and 2004 documented rising debt-to-income ratios even as real median household income stagnated, per Census Bureau data. The Bureau of Labor Statistics showed housing consuming roughly 33% of average household spending – and climbing.

Personal bankruptcies hit a historic peak in 2005, exceeding 2 million filings, just before the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) made filing significantly harder.

Warren's own research, published in Health Affairs (2005), found that medical problems contributed to approximately half of all personal bankruptcies filed in 2001. Her paper "The Growing Threat to Middle Class Families" (Brooklyn Law Review, 2003) documented that families with children were nearly three times more likely to file for bankruptcy than childless households – and roughly 40% more likely to lose their home to foreclosure.

"The cost of being middle class has shot out of the reach of the median family. For millions of families, the situation is getting desperate."

– Elizabeth Warren, Harvard Gazette, 2003

Deregulated consumer credit made it worse. As Warren described in Harvard Magazine (2006), easy credit had become "a monster that feeds on families in trouble" – allowing households to paper over structural budget gaps with credit cards and cash-out refinancing until the debt became unmanageable.

All Your Worth was written as a direct response to that structural trap. More children were living through their parents' bankruptcy than their parents' divorce, Warren noted in her SSRN paper. The formula that followed wasn't a lifestyle hack. It was a structural firewall.

What the Book Actually Says

How the Rule Appears in the Original Text

The book's central argument is that financial stability comes from balance, not deprivation. Warren and Tyagi rejected the dominant personal finance advice of the era – either extreme frugality (cut the lattes) or aggressive investing (pick the right stocks) – and proposed a structural reframe instead.

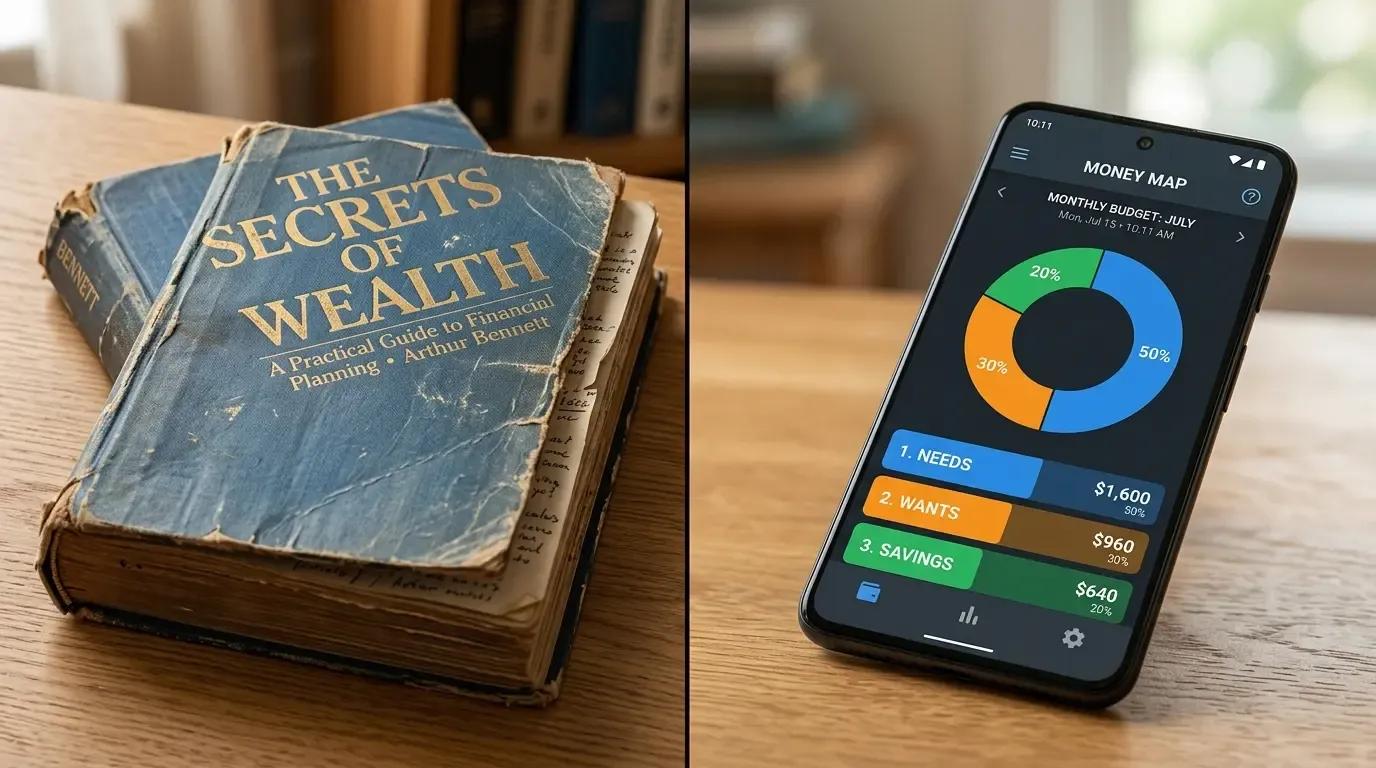

They called it the Balanced Money Formula. The three categories use specific terminology:

- Must-Haves (50%): Expenses you cannot avoid – rent or mortgage, utilities, groceries, minimum debt payments, insurance, basic transportation

- Wants (30%): Everything that improves your life but isn't survival-critical – restaurants, subscriptions, vacations, entertainment

- Savings (20%): Debt payments above the minimum, emergency fund contributions, retirement accounts

All percentages apply to after-tax income (take-home pay), not gross salary. That distinction matters: it's the money you actually see, not the number on your offer letter.

The authors used an analogy that clarifies the intent. Checking your budget against the Balanced Money Formula, they wrote, is like checking your cholesterol against recommended levels – it tells you whether you're in a healthy range, not whether you need to become a different person.

"Testing yourself against the Balanced Money formula is a little like checking your cholesterol against the recommended levels."

– Warren & Tyagi, All Your Worth (2005), as cited by Get Rich Slowly

The book's differentiation from contemporaries was meaningful. Where most financial guides of the era focused on investment selection or extreme coupon-clipping, All Your Worth focused on the structure of spending – specifically, on keeping fixed obligations (Must-Haves) below 50% of take-home pay. That ceiling on fixed costs was the mechanism Warren believed would prevent the bankruptcy spiral she'd spent years documenting.

Before the Balanced Money Formula, the dominant frameworks were the envelope system, zero-based budgeting, and the "pay yourself first" principle. All three required either granular tracking or a degree of financial discipline that overwhelmed households already stretched thin. Warren and Tyagi's contribution was a macro-level check: three aggregate categories, one percentage test, applied to the number you actually see in your bank account.

The Logic Behind Each Percentage

Must-Haves (50%): Why Half Your Income Has a Hard Ceiling

The 50% cap on necessities isn't arbitrary. It reflects Warren's empirical finding that families who committed more than half their income to fixed, unavoidable costs lost their ability to absorb income shocks. Once rent, car payments, and insurance consumed 60% or 70% of take-home pay, a single job loss or medical bill became a bankruptcy trigger.

The 50% ceiling functions as a structural safety margin, not a spending target.

According to Bureau of Labor Statistics consumer expenditure data for 2024-2025, the average American household allocates its spending roughly as follows across essential categories:

| Essential Category | Approximate Share of Total Spending |

|---|---|

| Housing (rent/mortgage + utilities) | ~34% |

| Transportation | ~17% |

| Food at home (groceries) | ~8% |

| Healthcare and insurance | ~8% |

| Total essential spending | ~67% |

That 67% figure versus the 50% target is the central tension in the rule's modern applicability – a point addressed directly in the criticism section below.

The gap between what the rule prescribes and what households actually spend on essentials is the most important number in this entire debate. It doesn't invalidate the framework. It tells you that the 50% ceiling is a diagnostic threshold, not a description of average American spending.

Wants (30%): The Difference Between a Need and a Want

The 30% category is where most budgeting systems either over-restrict – creating unsustainable deprivation – or under-define, creating confusion about what belongs where. Warren and Tyagi drew a clear line: a need is something you must have to maintain basic function; a want improves quality of life but isn't survival-critical.

The distinction isn't about judgment. It's about categorization for planning purposes.

| Category | Need | Want |

|---|---|---|

| Food | Groceries for cooking at home | Dinner at a restaurant |

| Transportation | Monthly transit pass | Daily rideshare to work |

| Housing | Rent, mortgage, utilities | Extra streaming subscription |

| Clothing | Durable seasonal footwear | Designer shoes for a special occasion |

| Technology | Functional smartphone for work/communication | Latest flagship model when current phone works |

| Leisure | Library book, free park visit | Concert tickets |

| Beverages | Water filter, tea bags | Daily coffee shop order |

| Vehicle | Basic insurance and fuel | Aftermarket alloy wheels |

The practical test: if you lost your job tomorrow, which expenses would you cut immediately? Those are wants. The ones you'd keep paying regardless are needs.

In practice, the need/want line shifts with income. A car payment is a need for someone commuting 40 miles to work in a city with no transit. It's a want for someone three blocks from a subway stop. The formula doesn't resolve that ambiguity for you – it forces you to resolve it honestly.

Savings and Debt (20%): Pay Yourself First

The 20% savings category operates on a specific principle Warren and Tyagi embedded into the formula: pay yourself first. The 20% comes off the top before discretionary spending decisions are made – not whatever's left over at the end of the month.

The category covers two things: debt payments above the minimum (accelerated payoff) and savings or investments (emergency fund, retirement accounts, other goals).

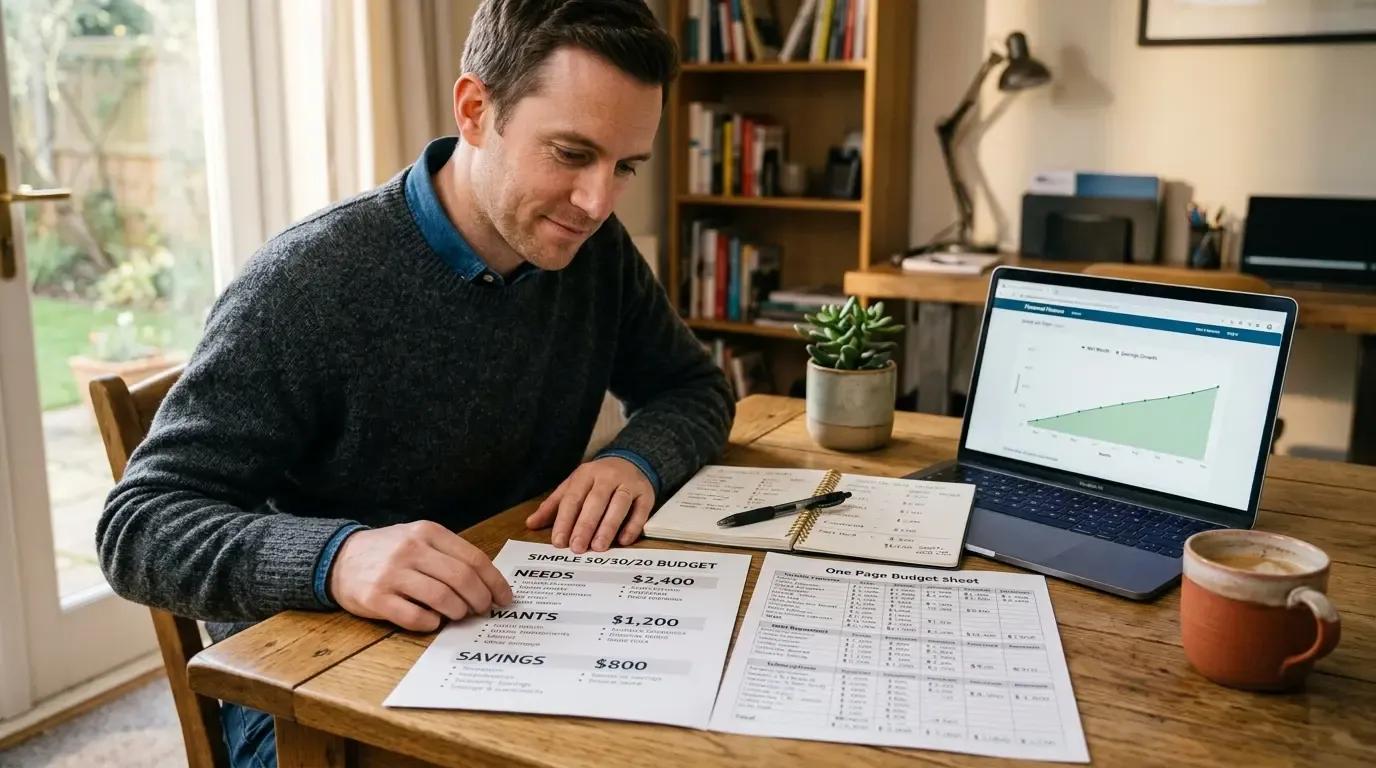

The table below shows how the formula translates across different monthly take-home income levels. These are after-tax figures.

| Monthly Take-Home | Must-Haves (50%) | Wants (30%) | Savings/Debt (20%) |

|---|---|---|---|

| $3,000 | $1,500 | $900 | $600 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $8,000 | $4,000 | $2,400 | $1,600 |

Budget allocation by the 50/30/20 rule across three U.S. income levels. All figures based on after-tax (take-home) income. The 20% savings column represents the minimum directed to savings and above-minimum debt repayment before discretionary spending is calculated.

If you're carrying high-interest debt and want to model how aggressively you could pay it down within this structure, the debt payoff calculator runs the numbers against your actual balances and rates.

One practical note: the 20% floor on savings is where the rule draws its sharpest criticism. For someone starting retirement savings at 40, carrying significant student loan debt, or living in a high-cost market, 20% directed toward savings and above-minimum debt payments may not close the gap. The formula sets a floor. It doesn't guarantee the floor is high enough for your specific situation.

How the Rule Spread After 2005

Media, Culture, and the Popularization Machine

The Balanced Money Formula left the pages of All Your Worth and entered mainstream financial culture in waves.

The first wave came from traditional media. In the late 2000s, following the 2008 financial crisis, personal finance coverage in Forbes, Business Insider, and Yahoo Finance began citing the 50/30/20 framework as a practical triage tool for households trying to stabilize after job losses and foreclosures. The crisis made Warren's bankruptcy research feel immediately relevant to millions of readers who had never heard of the Consumer Bankruptcy Project.

The second wave came from fintech. Budgeting apps like Mint, YNAB, and Chime built the three-category structure into their default interfaces. Major banks including Chase and Bank of America incorporated the rule into their financial wellness educational materials. By the mid-2010s, the rule wasn't just advice – it was the default architecture of how budgeting software organized spending data.

"People gravitate toward 50/30/20 because it's easy to remember and doesn't require complicated math... But the budgeting hack found a second life on TikTok, where videos about the rule have garnered millions of views – especially in finance-focused TikTok communities like #moneytok and FinTok."

The peak of media mentions ran roughly from 2014 to 2018, coinciding with the growth of YouTube personal finance channels and the explosion of fintech adoption. A second spike came during 2020-2021, when pandemic-era economic disruption sent millions of people searching for basic budgeting frameworks. Business Insider's 2024 coverage credits Warren and Tyagi directly for popularizing the rule, describing it as "a framework to track spending against" rather than a rigid prescription. By 2026, the rule functions as the default mental model for household budgeting across the English-speaking internet.

The rule's longevity comes down to cognitive load. Three numbers. Three categories. No spreadsheet required. Prudential Financial describes it as a "simple budgeting rule" that "many learned of... from Elizabeth Warren, who wrote about it in her 2005 book." That framing – simple, attributed, grounded in research – is exactly what made it teachable at scale.

Adaptations for Different Incomes and Regions

The formula's numerical proportions have been modified more than its three-category structure. No single author owns the adaptations the way Warren and Tyagi own the original – these are practical responses to economic conditions, documented across financial publications.

60/20/20 or 70/20/10 (High cost-of-living markets): For households in cities like New York, San Francisco, or Boston, where housing alone can consume 40%+ of take-home pay, financial advisors writing in Forbes and Investopedia regularly recommend shifting to 60% or even 70% for needs, compressing wants to 10-20%, and protecting the 20% savings allocation.

FIRE movement inversions (40/10/50): The Financial Independence, Retire Early community, popularized by bloggers including Mr. Money Mustache, flips the formula's priorities – targeting 50% or more toward savings and investments, with needs and wants sharing the remainder. This isn't a modification of the 50/30/20 framework so much as its philosophical opposite.

15/65/20 prioritization: Investopedia's 2026 coverage documents a variant where 15% goes to savings first – before calculating needs – 65% covers essentials, and 20% handles discretionary spending. The sequence change matters behaviorally: saving before budgeting essentials forces a different set of trade-offs than saving whatever remains.

"Check if it's possible to stick to the traditional 50/30/20 structure, or if you'll need to adjust it to 60/20/20 or a different breakdown."

For freelancers and self-employed individuals whose income varies month to month, applying fixed percentages requires a different approach entirely. The guide on budgeting for freelancers covers how to adapt percentage-based frameworks to variable income streams. And if you're weighing a full switch between methods, the case study on switching budget methods walks through what that transition actually looks like in practice.

Is the Rule Still Relevant in 2026?

The honest answer: the three-category framework holds. The specific percentages are under serious pressure.

A 2023 report from the Bank of America Institute found that inflation and rising credit costs pushed the average middle-income household's needs spending to approximately 65% of take-home pay – 15 percentage points above the rule's ceiling. A 2024 Harvard University study documented that in major U.S. cities, housing costs alone exceeded 40% of household income, making the 50% cap on all necessities structurally impossible for many renters.

CNBC's 2023 analysis was direct: "The 50-30-20 rule is a classic guideline for budgeting, but inflated costs mean that the math no longer works for most Americans."

Fidelity data from 2025 showed that more than 45% of millennials had abandoned rigid percentage-based budgeting in favor of app-driven flexible tracking. NYU Stern analysts proposed a modified 60/15/15/10 model (needs/savings/investments/wants) as a more accurate reflection of current economic conditions.

Yet the rule's conceptual core – cap your fixed obligations, protect your savings rate, allow yourself discretionary spending – remains the consensus starting point in financial education. Experian, Prudential, Transamerica, and the CFPB all continued to use it as a baseline framework in 2025-2026 materials, with the consistent qualifier that the percentages are a reference range, not a mandate.

"The 50/30/20 budget is just a recommendation; it's meant to be flexible, and to provide some structure within the real-world circumstances you live in."

For households with seasonal or unpredictable cash flow, the percentage-based approach needs additional scaffolding. The guide on seasonal income budgeting covers how to apply a percentage framework when your baseline income changes quarter to quarter.

Criticism and Limitations

The Low-Income Problem

The rule's most significant structural flaw is its inapplicability to households where essential costs exceed 50% of take-home pay before any discretionary decision is made.

Analysis of 2024 U.S. consumer data found that 42% of households in the lowest income quintile spent more than 60% of their income on basic necessities – housing, food, and transportation alone. For these households, the 50/30/20 rule doesn't describe a budgeting choice; it describes an income problem. No reallocation of percentages fixes a situation where fixed costs approach or exceed total income.

The same structural issue appears internationally. Eurostat data from 2024 showed that in Greece and Spain, housing costs alone exceeded 40% of disposable income for more than 30% of low-income households. Their realistic budget structure looks closer to 70/20/10 (needs/savings/wants) – and even that requires aggressive management.

The rule was designed for the American middle class facing a specific 2005 problem: fixed costs creeping upward while income stagnated. Warren's research in the Brooklyn Law Review (2003) documented that dynamic in detail. The formula was never designed for households below the income threshold where the math closes – and applying it there sets up unrealistic expectations rather than actionable guidance.

Universal Formula or Individual Framework?

Financial experts who critique the rule tend to target two specific weaknesses: the savings rate and the rigidity of categories.

The savings rate argument: The rule allocates 20% to savings and debt. For someone starting retirement savings at 40, carrying significant student loan debt, or living in a high-cost market, 20% may be structurally insufficient. The FIRE movement targets 50-70% savings rates. Veterans United's financial education materials note directly: "The main criticism of the balanced money formula is that it doesn't require you to save enough. Many people believe that spending 30 percent of your budget for things you want today compared to 20 percent for your future will leave you in bad shape when it's time to retire."

The category rigidity argument: Ramit Sethi (I Will Teach You to Be Rich) argues that fixed percentage buckets don't accommodate individual priorities. Someone who values travel over dining out, or fitness over entertainment, needs a system that reflects their actual values, not a predetermined allocation. Dave Ramsey prioritizes aggressive debt elimination over the rule's balanced approach, arguing that high-interest debt warrants temporarily collapsing the wants category to near zero.

A 2025 arXiv paper on household bankruptcy prevention compared the 50/30/20 rule against a "one-third rule" – allocating approximately 33% to savings and debt repayment – and concluded that the standard 20% savings allocation "may fall short for those with substantial obligations."

"In contrast, the 50/30/20 Rule's smaller allocation for savings and debt repayment may fall short for those with substantial obligations…"

– arXiv, Preventing Household Bankruptcy: The One-Third Rule in Financial Planning (2025)

The practical consensus among financial planners: use 50/30/20 to establish a baseline and diagnose where your money is going. Then modify it based on your actual debt load, income stability, and financial goals. If you want to stress-test your debt-to-income ratio before committing to any allocation, the DTI calculator gives you a clear read on how your current obligations stack up against your income.

For a structured diagnostic, the questions below help identify whether the standard formula fits your situation or whether a modified version – or a different method entirely – serves you better:

- Is your monthly income stable and predictable (fixed salary or consistent freelance revenue)?

- After paying essential expenses, does less than 50% of your take-home pay remain?

- Do you carry consumer debt or credit card balances with interest rates above 15%?

- Is your primary financial goal short-term and requiring aggressive saving (down payment within 12 months, for example)?

- Do you have financial dependents – children or family members you support?

- Do you manage your budget solo or jointly with a partner?

- Do your discretionary expenses vary significantly month to month?

- Could you direct more than 20% of your income to savings without material lifestyle impact?

- Are you self-employed or do you have irregular income streams?

If you answered yes to questions 2, 3, 4, or 9, a modified version of the formula – or zero-based budgeting – likely fits your situation better than the standard 50/30/20 split.

Frequently Asked Questions

Who actually created the 50/30/20 rule?

Elizabeth Warren and Amelia Warren Tyagi created the Balanced Money Formula – the original name for the 50/30/20 rule – and published it in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan (Simon & Schuster). Investopedia, Business Insider, Experian, and Prudential all attribute the rule's popularization to Warren and Tyagi. The concept is sometimes informally referenced as "Senatori, 2005," referring to Warren's later Senate career, but the book predates her Senate tenure by eight years.

When was the rule published, and where?

All Your Worth was published in 2005 by Simon & Schuster. The Balanced Money Formula appears throughout the book as its central organizing framework. The rule entered mainstream financial media in the late 2000s and peaked in media coverage between 2014 and 2018, with a second wave during 2020-2021.

Is the 50/30/20 rule based on scientific research?

The rule is grounded in empirical research but is not itself a peer-reviewed finding. Warren's academic work – including the Consumer Bankruptcy Project, her Health Affairs study on medical bankruptcies (2005), and her Brooklyn Law Review paper "The Growing Threat to Middle Class Families" (2003) – established the empirical foundation. The 50/30/20 percentages represent her applied translation of that research into a practical household framework. Investopedia and Miro Kredit both describe it as a "rule of thumb," not a scientific prescription.

How does it differ from zero-based budgeting?

The 50/30/20 rule provides a macro-level allocation framework: three categories, three percentages, applied to after-tax income. It requires minimal ongoing tracking. Zero-based budgeting (ZBB) requires assigning every dollar of income to a specific spending or savings category, so that income minus all allocated expenses equals zero. ZBB delivers more granular control and is more effective for aggressive debt payoff or irregular income, but demands significantly more time and discipline. MMBB's 2023 comparison describes ZBB as potentially "overwhelming," while 50/30/20 "promotes a balanced approach" with lower implementation cost.

For a detailed comparison of both methods – including when to use each and how to switch – see the zero-based budgeting guide.

Conclusion: What the 50/30/20 Rule Actually Changed

The 50/30/20 rule didn't invent budgeting. Envelope systems, zero-based budgeting, and "pay yourself first" all predate All Your Worth by decades. What Warren and Tyagi contributed was a specific structural insight – that the primary driver of middle-class financial collapse wasn't overspending on wants, but the unchecked growth of fixed, unavoidable costs – and a formula that made that insight actionable in three numbers.

That reframe was consequential. Before 2005, most popular financial advice targeted discretionary spending (the latte factor). All Your Worth redirected attention to the structural layer: your mortgage, your car payment, your insurance – the costs that don't flex when income drops.

Twenty years later, the three-category structure is embedded in fintech apps, bank educational materials, and financial literacy curricula across the U.S. The specific percentages are increasingly contested – and legitimately so, given that average essential spending now runs closer to 67% of household budgets than the 50% ceiling. But the framework's core logic remains the most widely taught starting point in personal finance.

For households evaluating whether to apply this rule or a more granular alternative, the Bromoney budget planner app lets you input your actual take-home pay and spending to see how your real numbers compare against the 50/30/20 structure – without requiring you to commit to any specific method before you understand your baseline.

Sources

- Warren, E. & Tyagi, A. W. (2005). All Your Worth: The Ultimate Lifetime Money Plan. Simon & Schuster. Google Books

- Warren, E. (2003). "The Growing Threat to Middle Class Families." Brooklyn Law Review. SSRN

- Harvard Gazette (2003). "Middle-class income doesn't buy middle-class lifestyle." Harvard Gazette

- Harvard Magazine (2006). "The Middle Class on the Precipice." Harvard Magazine

- Experian (2026). "What Is the 50/30/20 Budget Rule?" Experian

- Investopedia (2026). "The 50/30/20 Budget Rule Explained." Investopedia

- Investopedia (2026). "Why Some People Are Tweaking the 50/30/20 Budget Rule to 15/65/20." Investopedia

- Business Insider (2024). "What Is the 50/30/20 Rule: A Tool for Effective Budgeting." Business Insider

- Prudential Financial. "The 50/30/20 Rule and Budget." Prudential

- CNBC (2023). "Why the 50-30-20 budgeting rule is out of reach for most Americans." CNBC

- arXiv (2025). "Preventing Household Bankruptcy: The One-Third Rule in Financial Planning." arXiv

- Maps Credit Union (2025). "Revisiting 50/30/20 for 2026." Maps Credit Union

- Veterans United (2013). "The Formula to a Balanced Budget." Veterans United

- Get Rich Slowly (2008). "The Balanced Money Formula." Get Rich Slowly

- MMBB (2023). "Zero-Based Budgeting and the 50-30-20 Rule." MMBB

Read next:

Bromoney Team

Editorial team focused on practical borrowing guidance and financial planning.

- Editorial Board

Was this article helpful?

Same blogs

Installment Loans for Bad Credit: How They Work, Pros, Cons, and Smart Comparisons

Learn how installment loans for bad credit work, their advantages and risks, and how to compare offers safely.

Case Study: I Switched from 50/30/20 to Zero-Based Budgeting – Here's What Changed in 6 Months

A six-month documented case study comparing the 50/30/20 rule and zero-based budgeting – with real numbers, behavioral shifts, and an honest verdict on which method delivers more control.

When the 50/30/20 Rule Breaks Down: A Guide for Irregular Income, Gig Workers & the Self-Employed

The 50/30/20 rule was built for predictable paychecks. If your income fluctuates – freelance, rideshare, delivery, consulting – the percentages collapse the moment income dips. This guide breaks down why the rule fails gig workers and the self-employed, and lays out the budgeting systems that actually hold up: zero-based budgeting, Pay-Yourself-a-Salary, Profit First, and envelope allocation.